The unique reason some banks termed “too big to fail” could do just that, fail, in the coming years won’t be because of regulation, interest rates, or even being overleveraged …it’s because they’re failing to innovate and provide acceptable modern standards of User eXperience (UX).

Large financial institutions are ill. They are beginning to lose market share, perhaps even fail, because they have been far too complacent at providing efficient and engaging user experiences.

Banks may fail because of UX!? You’re joking right?

No. No I am not. That is exactly what I’m going to argue.

So how could UX be the causation for failure? Enter the increasing disruptive explosion of thousands of innovative financial technology, aka ‘fintech,’ startups.

Ironically it’s not just big banks who will falter. With Forbes estimating that there are 5-6,000 fintech startups globally, these fintech startups face the considerable challenge of competing against each other as well

…enter the still undervalued competitive advantage of superior UX

Speaking from a point of having spent the last few years of a 12 year long career in UX working and interviewing with NYC financial institutions, speaking with colleagues, and visiting with several fintech startups, I have gained a pretty unique analyst viewpoint into the current state of the financial industry. If I were a Doctor I would coin the existing industry condition as:

C.R.U.D.D. = Costly Recurring UX Deficit Disorder

Or the longer version of Costly Recurring UX Driven Development Deficit Disorder).

So with a medical analogy diagnosis let’s continue it by taking a walk through its Symptoms > Causes > and Treatments

SYMPTOMS:

Falling Stock Prices: Bank stocks are down in the last six months compared to the rest of the market and it will only get worse if they don’t start innovating and producing markedly improved user experiences for customers, clients, and employees.

From top to bottom: S&P 500, Dow Jones, JPM Morgan, BNY Mellon, Wells Fargo, Citigroup, Morgan Stanley, and Credit Suisse at the bottom not doing well at all

* Google Finance May 15, 2006

Market Share Loss: Market share losses have already begun and are projected to continue. Deloitte estimates a €22 billion loss in the payments market over the coming years. A recent article from Forbes covering a new study by Accenture is even more ominous: “estimates that Full service banks could lose 35% of their market share by 2020 and up to 25% of US banks could disappear completely!”

Apathy toward Stocks: Middle class American investors are throwing in the towel on stocks because they either: (A). lack the discretionary income to ‘play’ in the market and/or (B). have lost faith in the future of a stagnant market. Even pre-tax incentives don’t have as much appeal when individuals want to receive as much of their income as fast as possible since wages aren’t keeping up with inflation. The latest working generation of millennials don’t trust the stock market the stock market either; so this funk doesn’t seem to be short-lived.

Layoffs and Hiring Freezes: As early as March of this year I was told by at a friend in a mid-tier bank they had already decided to freeze hiring for the rest of the year.

Layoffs and Hiring Freezes: As early as March of this year I was told by at a friend in a mid-tier bank they had already decided to freeze hiring for the rest of the year.

And not planning to hire for the next 9 months is the good news! The bad news in recent years is layoffs are many and analysts only expect reductions to continue well into the next decade.

That chart at right don’t look good: Business Insider: “CITI: The ‘Uber moment’ for banks is coming — and more than a million people could lose their jobs”

Tech Project Cancellations and Freezes: In my brief time consulting in NYC I have seen several modernization projects either killed completely or put on hold. My experience isn’t an anomaly either. The Wall Street Journal documents an analyst lamenting that “overall anxiety levels are very high” because several detrimental business factors have left banks with just one major tool left for eking out profits …by cutting costs.

Reduced Employee Compensation: As CNN Money puts it …the party is over. In the previous year compensation costs were down 10% for one firm, 28% for another, and so on. Projections aren’t great for 2017 either. Definitely a negative effect on employee morale.

Reduced Trust and Loyalty: It’s no secret that Main Street thinks that Wall Street is grossly overcompensated from the message of Oliver Stone’s 1987 original ‘Wall Street’ movie to modern day Occupy Wall Street protestors.

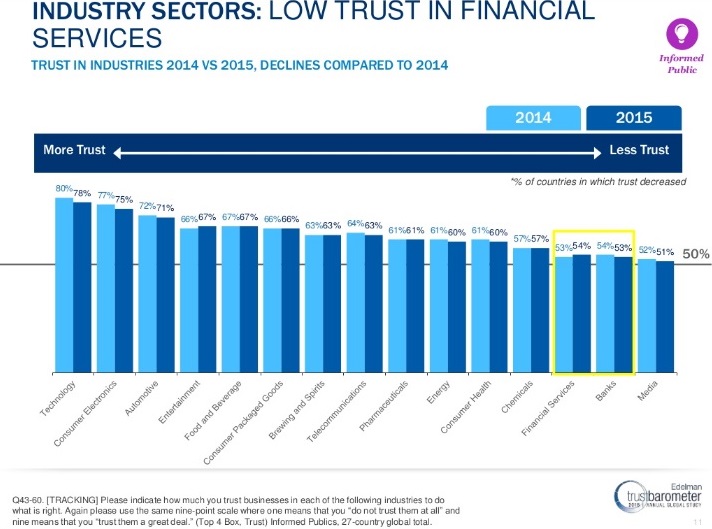

Lack of Trustworthiness: According to Edelman trust is slightly up for financial services in the last couple years however it’s second-to-last of all industries (below) ahead of only the media, yikes.

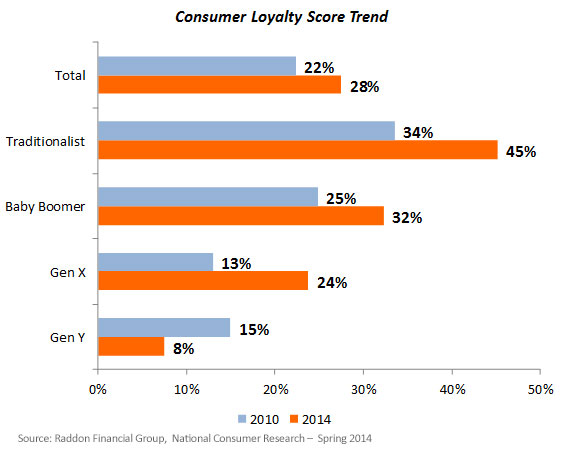

Eroding Future Loyalty: Raddon’s National Consumer Research concludes that although loyalty is ok for older generations, it has ‘disintegrated‘ (see chart below) for Gen Y as covered in ‘The Millennial Disruption Index.’ The report states:

“Thus, institutions are compelled to change their modes of customer engagement to attract and retain customers.” (cough, cough, UX)

CAUSES:

First it’s important to note there appears to be varying levels of C.R.U.D.D. severity in financial institutions and that some are in fact taking steps to rectify the problem (by creating semi-creative environments, increasing education, seeking new talent, etc). However even with these few steps, their efforts are still insufficient because they are not putting forth the full effort to avoid falling behind (technologically and perceptually) the status quo of today’s expected user experience. You see…

Banks aren’t just banks anymore …they are now software companies which specialize in banking.

The causes of C.R.U.D.D in financial institutions include:

Exponential Contemporary UX Expectations: For about a decade now modern society has come to experience increasingly more intuitive and efficient usability in their usage of personal computers, mobile devices, operating systems, apps, kiosks, and social networks. However financial institutions have failed to keep up with this rate of improvements. Millennials aren’t completely abandoning brick and mortar banks, but they are utilizing them less.

UX Immaturity: There are a few variations online regarding a UX Maturity model ranging from 6 to 8 steps. The common first steps of the models include lack of budget, hostility/ pushback against UX, decentralized design, lack of leadership, etc. Most large banks are only around halfway through the steps while most startups seem to be merely at stage 1 or 2.

UX Budget Lacking: Human Factors International (HFI) recommends that 10% of IT budget be allocated to UX. It is quite apparent in many companies that they’re not even at 5%.

UX lacking a Seat at the Head Table: To my knowledge, no major financial institution has a top level executive, or CXOs (Chief Experience Officers), focused solely on the role of improving user experience (for customers, clients, and employees) in the C-level suite like Apple’s Jonathan Ive. Saxo Bank, a small Danish investment bank, lead the way in 2015 by adding a CXO; where blue chip banks with their immense wealth and capabilities should have lead in creating this position. Similarly we don’t see Managing Directors level roles for UX either. I have only seen UX Director positions which are still 2 to 3 levels removed in hierarchy under a CTO. Because of that lesser rank they are plagued with constantly having to fight an uphill battle to evangelize the benefits of UX, maintain understaffed teams, and get Product Owners and Development Directors to include UX into their SDLC (Software Development Life-Cycles).

While banks can have CTOs and CIOs who have some familiarity, faith, and interest to see UX advanced at their companies and their roles may tend to include some elements of this goal; however they are increasingly pressed with technology, shareholder, fiduciary, regulatory, operating, labor, and other concerns to be able to stay up to speed with the latest developments and expectations in UX, as well as what it takes to meet those demands.

Too few Employed Designers: One large bank’s ‘Innovation Center’ I applied to had only one designer role approved …on a team of 30! News flash: Guess who’s not going to be very innovative then. Ironically, execs love, love, and I mean LOVE to point to Apple as a goal for the quality of design they want their teams to produce but fail to provide the relevant support. Former Apple design veteran Mark Kawano stated that Apple has roughly 100 designers. Don’t expect Apple design quality, if you aren’t willing to provide the proper number of design professionals to create quality solutions! (see 10% of IT budget above).

Design teams should include a healthy amount of specialists in design management, information architecture, UX design, UI design, graphic design, research, and front end devs. Special note to well-funded startups. Stop chasing unicorns and faux ‘rockstar’ designers because your overall design and services will suffer. Many of us designers are very good at several areas of design, however in this day and age of a plethora of information and programs, no one can be an all-around expert (highly proficient in all areas of design). And if one claims to be, they are either blissfully ignorant of reality, or a dirty rotten liar. Teams win championships; not individuals.

Too high a Developer to Designer Ratio: In addition to the above deficit of designers often there is a very high ratio of developers to designers. Some large companies have hundreds of developers and a paltry handful of designers. One startup I spoke to was building a trading service, complete with interface, and their team had 50 developers and zero designers…..zero! That’s beyond a poor decision. That’s downright negligence by the hiring (product) manager to the investors.

Siloed and Late Design Inclusion: Major departments will often have a six designers in wealth management, one in capital markets, and a few in trading all reporting to a department CTO (or below). Not only are they understaffed but they have no cohesive structure in place to ensure cross-pollination of ideas and promotion of universal design. And UX, at no fault to designers, is often incorporated in bank projects a day late and dollar short to make impacts that avoid wasted dev effort and provide usable software.

Outdated Interfaces and Data Visualizations: How efficient, accurate, and enthused do you think bank employees are still using excel spreadsheets to track and transfer data? Not very. They are time consuming to build, not standardized and thus only understood by a few, difficult for new novice users to learn how to use, and error prone.

Seeing one too many archaic interfaces in useage proved to me that design is still ignorantly considered by many in finance as just a ‘luxury’ inclusion, an afterthought of systems development to make things ‘pretty’ …art. But the reality couldn’t be further from the truth and decrepit examples like at right are costing banks $ millions in lost productivity, competitive advantage, and costly errors.

Dev from Scratch: Due to a lack of unified design, developers at banks are wasting HUGE amounts of time and effort creating custom (and crappy) interfaces. They are only now starting to utilize Javascript libraries to increase the speed of development but without a solid design team they still won’t achieve maximum efficiency in utilizing standard parts.

Fighting the Wrong Battle: So how are banks responding? They’re trying to stifle fintech startups with regulation. Bad move; more like wasting money on lawyers and lobbyists fighting against the tide of the inevitable technology revolution. It would behoove them to reference the taxi industry’s current losing battle against Uber and Lyft. These banks would be much better off at trying to utilize their wealth by beating fintechs at their own game …innovating and providing better UX.

Uninspiring Work Environments: Most of the working environments I’ve seen are still stuck in the dated thinking of needing to be onsite every day, chained to cubicles or plopped randomly into empty noisy trading floors seats or customer support agents.

Some execs naively think they can just hire people from ‘Silicon Valley’ (a magical fairy land where everyone is somehow far smarter). I have seen it happen twice. But the irony is people in New York and other parts of the country (many of their own already existing employees) are just as smart. The difference ironically is just that management is often not providing their existing offices with the kind of environment and culture that Silicon Valley companies provide their tech teams to be successful.

Misinterpreting and Implementing Modern Development Trends: Bank tech leaders read articles or hear about new development trends and will tout making projects ‘agile’ and to implement ‘lean ux.’ But things get lost in translation between the message and the reality. For example:

Agile: Often the word ‘agile’ is erroneously used as reference to work without any requirements whatsoever and/or is an excuse to provide only a skeleton crew. That’s not what makes agile methodology advantageous over waterfall at all.

It’s about creating a healthy productive working environment, with comprehensive cohesive multidisciplinary teams (supplemented by agile training and coaching) to more rapidly and flexibly development on a less cumbersome set of requirements (user stories) to produce more innovative products and services.

Mobile First: Responsive design is a very important aspect to consider in this day and age of multiple device sizes but frankly the honest reality is the great majority of the large banks audiences are users predominantly viewing on very large displays, not small mobile screens. When does mobile first make sense? For customers and senior bankers who frequently visit clients. But the lion share of users in banking are analysts, traders, and advisors who need a large real estate of pixels to do their job. Therefore it’s important to focus design for their needs from a standpoint of ‘Large Screen First.’

Lean UX: This is the theory that UX deliverables and waterfall process have become an isolated and cumbersome slowdown of progress slowing innovation. For managers looking to cut costs it sounds nice in theory, but applying a concept that might relate to some manufacturing, doesn’t equate to the reality of software UX design because:

A. UX is already Lean: I have never seen an environment that had the luxury of a ‘Supple/fat UX’ design process and timeline which had excess (countless months on just one project to obtain research understanding and design concepts before action). In reality UX designers are always working on multiple projects and/or dev teams are chomping at the bit for design plans with an already limited availability to conduct even a few select UX tasks from a designers toolbox.

B. Slow is smooth, smooth is fast. Meaning get the job (design) done properly the first time. This absolutely doesn’t mean to overanalyze before taking action. It means there is still the danger of acting too fast which can ironically end up delaying progress far more so than conducting proper due diligence. For example when dev teams have to go back and rework far too many elements because of hastily made decisions; it’s a huge detriment to budgets and morale. UX deliverables ARE needed to produce an optimum design solution. UX tasks/deliverables provide immense benefits to provide the best holistic design the first time around. Most UX tasks should still be planned in a waterfall manner, but also customized and aligned in a hybrid manner to support the modern needs of dev sprints and releases.

In my opinion this theory is a harmful misnomer to sell books by advising management to pressure making, what is already in reality a lean practice, emaciated and ineffective to properly influence necessary optimal and timely impactful changes.

Fintech Startups: Finally, a lot of innovative and capable people have seen banks faltering to modernize and have decided to throw their hat in the financial arena. These startups are flush with cash and fresh perspectives. Disruptive fintech’s are now mostly small B2C oriented companies but they will undoubtedly continue to grow into the B2B realm.

TREATMENT:

But don’t fret Brian Moynihan, Michael Corbat, Ken Chenault, Tidjane Thiam, Jamie Dimon, and James P. Gorman, etc. there IS a treatment to CRUDD in your systems! Banks today need a series of additions and improvements to their tech departments to improve their UX Maturity and create an optimal creative ecosystem that can ensure they don’t lose market share and instead gain consumer edge which increases customer satisfaction …and profit. With the aforementioned love of referencing Apple design, executives also need to champion what Kawano states:

“It’s actually the engineering culture, and the way the organization is structured to appreciate and support design.”

Examples how banks can grow to provide the culture necessary to reduce customer service calls, increase speed of transactions, increase employee morale, increase customer satisfaction, loyalty, and profit include:

UX Budget Lacking: As stated previously budget spent on UX should be around 10% of the entire IT spend.

Executive Level Unifying Leadership: A CXO (Chief Experience Officer). This growing addition to corporate officer cadre coordinates efforts to advance the experience and performance of products and services from the human perspective. The CXO champions and orchestrates across the entire company to improve the customers’ (and employees’) experience in modern corporation’s lifecycles. It is critical that this role have gravitas, higher than the status quo ‘UX Director,’ to truly ensure that experience needs are being met and promoted just as strongly as finance (CFO), Operations (COO), Marketing (CMO), Technology (CTO), etc. Without a doubt in this modern climate of demanding human wants and needs, their ability to gain advantage over their competition will slip if they don’t add an executive experience design officer position.

Department UX Heads: Reporting to the CXO should be X number of Director/VP level UX Heads who lead small teams that focus on the experience of a particular institution department or branch. The members in these teams are focused on a niche comprehension of their assigned department/branch to excel in improving these very complex financial fields.

Creative Environment: A design team should have a positive, bright, clean space with bountiful wall and whiteboard space in which to share visual concept work and hash out improving complicated use cases. Unlike many professions, designers absolutely require quiet time to really think through problems. An open desk environment does promote dialogue and sharing; however there should still be ample closed off rooms for pinning up ideas and offering a quiet retreat which designers can head to focus on solving problems and sketching out solutions. FastCodeDesign has a solid write-up going into the subject in greater detail focusing on Google Ventures fostering creativity via a Design team ‘War Room’ (below). And while you’re at it add standing desks to boost productivity by 46%.

Creative Environment: A design team should have a positive, bright, clean space with bountiful wall and whiteboard space in which to share visual concept work and hash out improving complicated use cases. Unlike many professions, designers absolutely require quiet time to really think through problems. An open desk environment does promote dialogue and sharing; however there should still be ample closed off rooms for pinning up ideas and offering a quiet retreat which designers can head to focus on solving problems and sketching out solutions. FastCodeDesign has a solid write-up going into the subject in greater detail focusing on Google Ventures fostering creativity via a Design team ‘War Room’ (below). And while you’re at it add standing desks to boost productivity by 46%.

A Skunkworks: Even more so the future of banking will include some aspects of virtual reality, haptic technology, block chain, multi-modal authentication biometrics, etc. For example the ability to look at a financial situation in 3D is likely going to be far superior to the still dated 2D interfaces which just overload a banker or trader with numbers. A Fortune 500 bank should have it’s own small R&D department to keep it at the forefront of the industry.

Power Nap Acceptance: Remember George Costanza’s hilarious pursuit to remodel his desk to support his napping?

It’s actually not a joke. In addition to famed innovators such as Leonardo Da Vinci, Ben Franklin, Thomas Edison, Buckminster Fuller, and NASA utilizing polyphasic sleep, there are a number of studies proving that quick naps are beneficial to increased creativity and alertness. This reality is becoming more accepted, even promoted with sleep pods, in forward thinking companies looking to boost productivity. So don’t be a troglodyte, provide a small space and/or acceptance for employees to get in a quick reboot.

It’s actually not a joke. In addition to famed innovators such as Leonardo Da Vinci, Ben Franklin, Thomas Edison, Buckminster Fuller, and NASA utilizing polyphasic sleep, there are a number of studies proving that quick naps are beneficial to increased creativity and alertness. This reality is becoming more accepted, even promoted with sleep pods, in forward thinking companies looking to boost productivity. So don’t be a troglodyte, provide a small space and/or acceptance for employees to get in a quick reboot.

Design Talent: A bank should have a healthy mix of long term salaried designers and short term contractors. Learning and gaining a thorough understanding of complex financial lines of business (wealth management, home loans, sophisticated trading, etc) is a shallow learning curve [yes I said shallow (slowly obtained), not the often misquoted steep (or rapid) learning curve]. The salaried employees benefit the bank by providing the sage knowledge required to operate in a particular complex and highly regulated system while the contractors (often from other industries) provide fresh insight and different perspective on how to improve UX for a line of business.

A Low Dev to Designer Ratio: A lower ratio of developers to designers. For projects with a human interface element there ought be much lower (such as around 5 to 1, some even say 1 to 1, but never should it be beyond a 10 to 1) ratio. A lower ratio not only promotes a better user experience, it can also lead to far better project performance by ensuring that the design is closest to what’s needed the first time and thus reducing developer rework. A style guide helps guide consistency; but it’s not the optimal solution to providing best in class UX …actual design bodies are.

* Rule is for user facing products and services. Back end system projects predominantly requiring only back-end developers could be excluded from this rule of thumb.

Increased Proximity: Proximity increases collaboration and quality. To my understanding all of Apple’s designers are in one location (they aren’t spread across in 3 to 5 different countries and time zones). Still the latter can be the reality in a larger global corporation and can be beneficial in providing alternative ideas, however occasional visits and frequent videoconferencing is clutch to help build camaraderie, empathy, and sharing of ideas.

Focus on Service Design: Design efforts today need to expand beyond the realm of an interface. They must look at the experiences that occur across an entire ecosystem, or lifecycle. How does the marketing teams’ adverts relate to the onboarding of a customer and what they see on the registration page? How are unique situations and advisories provided to a client that only cares about X, and not information overload of the Y & Z? Is there an optimal comprehension of status between stages of a lifecycle? Having senior design leadership and service design efforts work to destroy barriers and bridge the gaps between costly siloed experiences where client attrition occurs.

Sustainable Development: It is the responsibility of the modern day designer and developer to work together to create efficiencies in the development process. Some examples of this include creating well thought out, but simple, reusable templates that developers can quickly apply to build uniformly designed content, dashboards, etc. Designers and developers must be afforded with free time and training to get better acquainted with legitimate agile training and benefits of newer technology such as JS libraries, githubs, etc.

Key Performance Indicators: You won’t know where the biggest financial gains can be made unless you provide a research element of a design team (working with PMs and SMEs) time to investigate where the service inefficiencies and low quality perceptions lie. Once a baseline is set regarding operational costs, human error costs, regulations maintenance, fine avoidance, time to tasks, loyalty, and customization perception, etc.; then it is the responsibility of a modern day design team to provide leadership with metrics and analysis regarding how UX design is helping to support the company’s bottom line and where improvements can be made. Because in the coming future banks will need all the help they can get to make even an online experience seem like the company truly knows, and gives a damn, about the customer.

Finally. What’s not needed …a Usability Lab: The decent budget chunk of money required to create a dedicated usability lab is typically not necessary and the results could be skewed because of the sterile environment. Better to evaluate users in the actual environment they’ll be using your products and services and only spend budget on usability testing assistive services such as usertesting.com.

But, but …what about the cost of building and maintaining such a team!?

Maintaining such a UX team and culture on par with standard large software companies could cost in the vicinity of:

- $ 0.5-2 million in non-recurring costs to create the appropriate environment

- $4-6 million in employee costs per year (30-60 designers). And this isn’t likely to even be 10% of the IT spend recommended.

The justification for this spend can be achieved either by:

- reducing or ‘rightsizing’ a few senior investment banker salaries.

- considering the increased revenue and/or savings as a small investment price to pay for business module as described above that could likely benefit a ROI in the neighborhood of tens, or hundreds of millions of dollars (perhaps even in the $ billions).

- Revenue-wise better UX will attract and maintain a greater market share and profit

- Savings-wise better UX can increase employee productivity and avoid human error or regulatory fines and penalties by better deterring illegal activity ($204 Billion in fines as a matter of fact since 2009, ouch!) as well as help to reduce costly overhead.

* It’s in this arena of UX’s financial benefit that it’s UX design professionals jobs to get better at promoting the business gains of their contributions through KPIs (more on that topic in my next article).